Many people feel their credit scores do not fully reflect their financial situation. Since the inception of credit scores, a person’s ability to achieve major life milestones, such as purchasing a home or starting a business, has been heavily reliant on a three-digit numerical value (i.e., credit scores). Although traditional credit scoring models (e.g., FICO) have provided a means for many individuals to achieve long-term success, they may also overlook important aspects of a consumer’s overall financial well-being.

For example, perhaps you are a consistent rent payer with a long history of timely payments; however, those payments will likely have no impact on your credit score. Additionally, as a freelancer, your steady income may appear unstable when viewed through the lens of an antiquated credit scoring model.

As a result, according to industry data, millions of financially responsible consumers are excluded from accessing affordable credit solely because their financial histories cannot be easily categorized within the narrow parameters of traditional credit-scoring models. The exclusionary nature of these credit scoring models appears to disproportionately affect young consumers, immigrant populations, and individuals who earn money in non-traditional ways (e.g., through the gig economy).

What if there were more equitable and advanced alternatives to traditional credit scoring methods? This is the central premise of advanced artificial intelligence (AI) credit-scoring models. Advanced AI credit-scoring models go beyond analyzing historical debt repayment behavior and incorporate a broader set of relevant data points to provide a more comprehensive and accurate financial profile.

The ultimate goal of advanced AI credit scoring models is not merely to develop a more sophisticated method of evaluating an individual’s creditworthiness, but rather to establish a system that provides greater fairness by enabling users to demonstrate their financial capabilities.

Summary

The article explains how artificial intelligence is used in credit scoring and how it can deliver fairer, more advanced lending decisions than older methods (such as FICO). Older methods use most or all of your credit history—your payment history, the amount you owe, how long you have had credit, whether there are recent inquiries, and what type of credit you have—to determine whether you qualify for a loan.

However, these older methods may omit significant components of a borrower’s financial picture, particularly for borrowers who do not fit a defined category (e.g., renters, freelancers, young people, immigrants) because they may not have a “thin” credit file.

The article describes how machine learning is used by AI to identify trends in previous loans and to create a more detailed, forward-looking picture of the risks involved in lending. It also describes how AI has the capability of including “alternative data” that old scoring systems do not include when determining credit worthiness (on time rental and/or utility payments, cash flow from your bank account, etc., and other stability indicators), therefore providing a predictive form of credit scoring that will focus on a borrowers’ ability to pay back a loan in the future rather than their history of borrowing in the past.

#Transformative AI for Clinical Decision: Empowering Doctors to Think Faster

Finally, the article discusses one of the major challenges of AI-based credit scoring: it inherits biases and discrimination from historical lending data and can also discriminate indirectly through proxies such as ZIP codes. To avoid this, the article emphasizes the need for fair testing, transparent “explanation” of how decisions are made (explainable AI), and regulatory oversight of AI credit-scoring methods, governed by laws such as the Equal Credit Opportunity Act.

In conclusion, the article states that AI credit scoring methods can help increase access to loans, provide more realistic second chances for people who have had past difficulties, and improve the speed at which lending decisions are made; however, this can only happen if the development of AI credit scoring methods is done so in a manner that includes strong transparency and governance to ensure fairness.

The Old Recipe: What Your Traditional FICO Score Sees (and What It Misses)

Traditional credit scores – think of them as a recipe for success – the most common recipe is based on a formula developed in the 1950s and still used today to evaluate your financial history using only five key ingredients:

1. Paying bills on time

2. The total amount you owe

3. The length of time that you have been using credit

4. The number of new applications you have made for credit

5. The mix of credit types (cards, loans, etc.)

The problem with this older approach to recipes, however, is that it looks backward. Recipes in their current form are mostly based on the way you were involved with debt in the past. That’s why a FICO score is a history report. Therefore, the traditional method does not include all aspects of your financial life today.

Therefore, many people who use money responsibly are excluded from the discussion. For example, a college graduate has a good job, but has never had a credit card; a freelancer has an average monthly income, but it fluctuates. These individuals have what some call a “thin” credit file. They do not have the correct number of right ingredients to make the traditional recipe, yet they are fiscally sound. Here, the idea of using AI to improve financial inclusion becomes viable by providing a more comprehensive view.

AI Credit Scoring: AI evaluates borrower risk using intelligent data analysis

Lenders are replacing reliance on a limited set of traditional credit scoring factors with AI-driven data evaluation. By combining traditional credit-scoring factors (payment history and utilization) with a broader set of permissible signals and applying machine learning, AI Credit-Scoring models can identify patterns in lenders’ credit data that predict future repayment trends. The end result will be a risk assessment that is quicker, more consistent, and provides a better picture of an applicant’s current financial position.

AI Credit Scoring cleanses and standardizes all inputted data; handles missing values; creates new features based on existing data (i.e., creating stability indicators as a result of cash flow timing or trend-based measures resulting from past account behaviors); trains models on historical loan defaults to create a probability of future default/delinquency and calibrates scores to reflect clear and understandable risk levels.

Once deployed, AI Credit Scoring models are continuously reviewed for potential “drift” (e.g., changes in consumer behavior or economic conditions) so the model’s performance does not degenerate without notice.

A key promise of AI Credit Scoring is improved decision-making. The use of AI in Credit Scoring has the potential to provide a more consistent decision-making process than humans and expand credit access for individuals with limited or no credit history (“thin file”), provided AI Credit Scoring can identify reliable indicators of an individual’s creditworthiness.

However, there are many ways to govern AI Credit Scoring to avoid exacerbating prior inequities. To prevent this from happening, lenders must implement robust data protection and ensure that prohibited characteristics (e.g., race, gender) are excluded from their scoring models; lenders must regularly test for disparate impact; they must use methodologies that provide explanations for how their models arrived at particular credit decisions; and they must conduct regular audits of their models.

In addition, lenders must provide consumers with clear, understandable explanations for why their applications were denied and must maintain consumer privacy and protect their personal information in accordance with federal and state laws.

AI Credit Scoring provides several benefits to lenders, including faster loan approvals, more accurate loan pricing, and early identification of risk factors that enable lenders to set credit limits and interest rates, and to trigger reviews to monitor borrower repayment with greater precision. Additionally, AI Credit Scoring may benefit borrowers by enabling faster loan approvals and potentially opening additional avenues for qualification when they do not meet traditional lending criteria, leveraging compliant alternative data to provide a clearer picture of the borrower’s ability to repay.

If implemented correctly, AI Credit Scoring will help align the lender’s approach to managing credit risk with fairness by providing a more transparent, easily auditable process for making credit decisions based on large datasets.

The Master Chef’s Approach: How AI Creates a 360-Degree View of Your Finances

The “old” traditional recipe for evaluating how risky an applicant is to lend money to was replaced by the “new” AI credit model that functions similarly to a “master chef” learning about a “new” type of food (cuisine) versus simply being given a set of “instructions.” Rather than using a fixed “recipe,” the AI credit model analyzes “thousands” of previous loans, some of which were repaid successfully and others that failed.

As part of its “machine learning” credit analysis, the system is able to identify subtle “patterns” of behavior that would be missed using a simple “formula” and builds a more detailed and comprehensive profile of the characteristics that determine whether an individual will be successful in repaying their loan.

This enhanced AI approach also provides the ability to analyze a much broader range of financial data and “information” than simply the applicant’s “debt history.” Experts refer to these additional sources of financial information as “features.” Examples of features to consider include: stability of the applicant’s income; payment history for rent and/or utilities; positive net cash inflows from the applicant’s bank account(s); etc. Ultimately, the objective of developing AI credit-scoring models is to provide a comprehensive “financial story” of the applicant, rather than simply a summary of their “debt.”

As such, AI credit scoring represents a fundamental shift in the evaluation process, from past performance to future potential. As a result of having access to a broad range of historical financial data and having the capability to evaluate all of the available data in a holistic manner, the AI system can develop an informed estimate regarding the applicant’s ability to repay the new loan – a process referred to as “predictive credit scoring.”

In short, while the AI credit system previously analyzed the applicant’s past financial activity, it now focuses not solely on where the applicant has been, but also on where they are going financially. This significantly expanded view of an applicant’s financial situation is enabled by a large volume of previously unavailable financial data.

Advanced Credit Analysis: Advanced analytics improve credit evaluation accuracy

Advanced Credit Analysis is changing how lenders assess creditworthiness by leveraging more data, improved statistics, and faster lending decisions. As opposed to assessing creditworthiness based upon a limited number of summary indicators, Advanced Credit Analysis examines patterns over time, such as income and expense stability, usage history, payment histories, and early signs of financial distress, so that lenders may distinguish temporary fluctuations in borrower payments from true underlying risk.

When combined with effective governance, Advanced Credit Analysis can provide more accurate credit risk assessments and enable consistent lending decisions across large borrower portfolios.

The primary impetus for Advanced Credit Analysis has been the adoption of machine learning and the need for robust validation. Machine Learning models are developed using historical data of repayment performance, validated through testing of those models on “hold-out” samples, and stressed through simulation of various economic environments.

This is typically the area where AI Credit Scoring plays: analyzing multiple relationships among variables, identifying potential or new predictors, and continually updating a lender’s risk assessment of a borrower as the borrower’s behavior changes. Additionally, Advanced Credit Analysis includes detailed design of features used in the analysis (e.g., volatility calculations, rolling averages), calibration of score bands, and ongoing monitoring for model drift, so the lender knows whether their systems continue to perform as the marketplace evolves.

Advanced Credit Analysis improves the precision of credit evaluations by supporting better segmentation and pricing of lending products through operational use. Lenders can adjust their credit limits, interest rates, and review processes based on each applicant’s risk profile, thereby reducing losses without tightening credit standards for all applicants.

Additionally, Advanced Credit Analysis enables rapid loan application processing by automating underwriting tasks and allowing the lender to prioritize those requiring human review. This process benefits lenders by enabling them to rapidly approve loan applications during periods of high volume.

For consumers with thin files or newly banked accounts, Advanced Credit Analysis may include permissible alternative signals and trend data. This enables lenders to evaluate a consumer’s ability to repay more fairly and transparently than traditional methods.

For Advanced Credit Analysis to be considered trustworthy, it must provide explanations and be auditable. Lenders will require clear reason codes to explain why a consumer was denied credit, documentation of the data used in the evaluation, testing for bias and disparate impact, and periodic performance reports. By establishing these controls, AI Credit Scoring can become a useful tool in an overall risk management system, rather than a “black box.”

When done properly, Advanced Credit Analysis and AI Credit Scoring can produce more precise, quicker, and less vulnerable to disruption credit decisions for both lenders and eligible borrowers.

Credit Risk AI: AI predicts the likelihood of loan default

Credit Risk AI enhances lenders’ ability to assess creditworthiness by converting large, complex datasets into probability-based risk estimates. Unlike using historical data in a static format, Credit Risk AI evaluates trends and behaviors in real time—including payment history, usage changes, cash flow, and early warning signs—to identify which borrowers may struggle to adapt as their financial circumstances change. With strong validation, Credit Risk AI improves the accuracy of lenders’ decisions and reduces inconsistencies among underwriters.

From an algorithmic standpoint, Credit Risk AI uses machine learning to model relationships between borrower characteristics and prior performance metrics, such as delinquencies, charge-offs, and cure rates. The data is cleaned, normalized, and processed for feature engineering (e.g., volatility scores, trend indicators, and interaction effects). The resulting features are used to train and calibrate models, ensuring the output falls within a defined risk band.

In many lending architectures, AI Credit Scoring is the client-facing manifestation of the underlying Credit Risk AI process; it transforms predictive signals into a score/rating that can be used to approve loans, set lending limits, and set interest rates. Together, Credit Risk AI and AI Credit Scoring enable lenders to transition from “all-or-nothing” rules to more granular risk segmentation.

Operationally, Credit Risk AI enables lenders to approve loans and manage their loan portfolios more efficiently. With Credit Risk AI, lenders can use predictive default probabilities to assess whether applicants are qualified for funding, set loan terms based on applicants’ risk levels, and initiate communication with borrowers whose creditworthiness has deteriorated since previous assessments.

Credit Risk AI also facilitates review processes through automated approval of low-risk applicants; automatic routing of applicants who are borderline for a lender to assess; and documentation of relevant decision-making factors that supported a lender’s decision to either approve or deny an applicant.

Over the life of the loan, Credit Risk AI enables lenders to continuously monitor borrowers’ performance against economic fluctuations and changes in borrowing behavior. This is critical because a model used to make credit decisions for borrowers’ needs must be periodically recalibrated/re-trained to remain effective/valid.

Because credit decisions directly affect consumers, there are governance issues associated with the use of AI Credit Scoring systems. Credit Risk AI should be designed to exclude prohibited variables; safeguard consumer data and privacy; and test for disparate impact (i.e., whether AI Credit Scoring systems disproportionately discriminate against protected groups). Methods that provide explainability and clearly documented rationales for adverse actions help ensure that AI Credit Scoring systems are understandable and compliant.

As long as Credit Risk AI is designed with transparency, monitoring, and fairness checks, it is a viable method for lenders to better identify and predict default risk while maintaining accountability and defensibility in the lending process.

Predictive Credit Scoring: Predictive models forecast future borrower behavior

Predictive Credit Scoring is an approach for assessing a customer’s likelihood of paying their debt in the future, using statistical models, machine learning, and predictive modeling. This model does not simply assess the credit profile at a single point in time; rather, it examines the customer’s credit profile over time, including trends in payment history, credit utilization, changes in credit mix, and other indicators of potential financial stress to determine their creditworthiness.

When executed properly, Predictive Credit Scoring enables lenders to make more accurate, consistent, and timely lending decisions based on a borrower’s current and past behaviors.

The first step in building a Predictive Credit Scoring model is to collect and prepare the data for analysis. This includes collecting traditional bureau variables, including internal data permitted under applicable law, such as account activity, transaction details, and repayment histories. Once collected, features are engineered to identify whether the trend is stable or trending in a particular direction (e.g., “the customers’ credit utilization has been increasing for six months” or “the income deposited into the customers’ accounts has become inconsistent”).

The features are then used to train a model on historical outcomes. Many of today’s applications leverage artificial intelligence credit scoring (AI Credit Scoring) to identify complex relationships between multiple variables and to generate updated risk assessments for each customer. Therefore, Predictive Credit Scoring is not limited to origination; it can be applied throughout the life of the loan to anticipate changes in the customer’s risk profile.

Predictive Credit Scoring provides lenders with a greater ability to segment and price their products. They can therefore set credit limits, interest rates, and approval thresholds based on predicted risk to reduce overall losses without denying consumer applications by tightening lending criteria.

Additionally, AI Credit Scoring enables faster decision-making by automating approvals for low-risk applicants and referring borderline applications to human reviewers. Furthermore, predictive credit scoring enables proactive portfolio management over time, including early intervention strategies (e.g., reminders, hardship options, etc.) before serious issues arise. As such, AI Credit Scoring is not only a tool for underwriting; it can also serve as a resource to support customers over the long term and manage potential risks associated with those relationships.

Since predictive credit scoring directly affects consumers, governance is an important consideration when using this technology. The models developed using predictive credit scoring should be regularly monitored for “drift” (i.e., changes over time), they should be validated across multiple economic conditions, and testing should be conducted to determine if there are disparate impacts on various groups of people.

Tools that enable explainable decision-making and provide consumers with clear explanations for why they were denied a loan or credit product will help ensure transparency and compliance when using AI Credit Scoring. When combined with appropriate consumer data protection policies and regularly audited, both predictive credit scoring and AI Credit Scoring provide a framework for responsibly forecasting behavior—enhancing prediction reliability while maintaining accountability for decisions.

Machine Learning Credit: Machine learning improves scoring models over time

Predictive Credit Scoring provides lenders with a greater ability to segment and price their products. They can therefore set credit limits, interest rates, and approval thresholds based on predicted risk to reduce overall losses without denying consumer applications by tightening lending criteria. Additionally, AI Credit Scoring enables faster decision-making by automating approvals for low-risk applicants and referring borderline applications to human reviewers.

Furthermore, predictive credit scoring enables proactive portfolio management over time, including early intervention strategies (e.g., reminders, hardship options, etc.) before serious issues arise. As such, AI Credit Scoring is not only a tool for underwriting; it can also serve as a resource to support customers over the long term and manage potential risks associated with those relationships.

Since predictive credit scoring directly affects consumers, governance is an important consideration when using this technology. The models developed using predictive credit scoring should be regularly monitored for “drift” (i.e., changes over time), they should be validated across multiple economic conditions, and testing should be conducted to determine if there are disparate impacts on various groups of people.

Tools that enable explainable decision-making and provide consumers with clear explanations for why they were denied a loan or credit product will help ensure transparency and compliance in the use of AI Credit Scoring. When combined with appropriate consumer data protection policies and regularly audited, both predictive credit scoring and AI Credit Scoring provide a framework for responsibly forecasting behavior—enhancing prediction reliability while maintaining accountability for decisions.

A significant advantage of Machine Learning Credit is its ability to continually evolve. As lending portfolios grow and repayment information becomes available, models will need to be revalidated to account for changes in fraud patterns, new products introduced into the market, and other factors that could lead to model drift. This enables greater consistency and accuracy in AI Credit Scoring, regardless of the segment of the marketplace being addressed at a given point in time or under changing conditions.

Additionally, Machine Learning Credit enables lenders to make more informed operational decisions, such as automatically approving low-risk applicants, prioritizing high-risk applicants for manual review, and alerting lenders to potential risks in an applicant’s current credit relationship before extending additional credit.

However, the development, deployment, and ongoing operation of Machine Learning Credit require governance. Lenders must have documentation of their data lineage, privacy protections, and compliance checks to ensure their models do not use restricted attributes or proxies that could lead to unequal treatment of applicants. Lenders should regularly perform fairness testing, monitor model performance, and provide transparency into their models’ decision-making processes (e.g., feature-importance reporting and reason code explanations).

The combination of these three types of measures will enable lenders to develop and maintain AI Credit Scoring solutions that are transparent and defensible. When coupled with appropriate oversight, Machine Learning Credit enables lenders to continuously improve their scoring models, manage risk more effectively, and provide qualified borrowers with easier, more predictable access to credit.

Credit Scoring Technology: Technology enhances fairness and transparency in lending

Credit-scoring technology continues to evolve beyond traditional approaches to make credit decisions more equitable, transparent, and consistent. Modern Credit Scoring Technology incorporates improved data management, enhanced model governance, and clearer explanations of each lender’s decision when determining whether to lend to potential borrowers based on their evaluation of borrower characteristics.

As long as it is used correctly, Credit Scoring Technology limits the use of ad-hoc judgment when making credit decisions and promotes the repeatability of credit decisions across different locations (branches), delivery channels (channels), and underwriters.

One major difference with modern Credit Scoring Technology is its capacity to track borrower behavior and identify patterns over time, rather than taking a snapshot at a single point in time. The systems can track how a borrower has historically managed payments, how consistent their credit utilization has been, and whether there are early indicators of financial difficulties, and translate these behaviors into risk estimates. This is an application area for Artificial Intelligence (AI) Credit Scoring technology.

Machine learning models can identify complex relationships in large datasets, estimate the probability of various types of risk, and enable faster credit decisions. In practice, AI Credit Scoring is most commonly integrated into a larger Credit Scoring Technology platform that includes data pipelines, validation checks, and policy-based rules that convert AI Credit Scoring predictions into approved loan amounts, interest rates, and/or loan limits.

Fairness and transparency require more than just accurate credit scoring. A strong Credit Scoring Technology will include key features such as bias testing and disparate impact monitoring, along with tools to prevent prohibited (or close proxies) variables from affecting the decision outcome. Additionally, it should support explainability by providing lenders with clear reason codes and simple summary information that helps borrowers understand the factors that led to their decision and what they need to do to potentially become eligible in the future.

Explainability is critical to developing successful AI Credit Scoring technology and to producing understandable, auditable results from the models. When an organization builds explainability into its Credit Scoring Technology, model insights become decision-rational for customers and ready for use in decisions.

Monitoring ongoing activity is another primary feature of Credit Scoring Technology. The technology enables organizations to monitor how their models perform, detect when underlying economic conditions have shifted enough to cause “drift,” and prompt them to recalculate and retrain their models to maintain stable results.

This will ensure that an organization’s use of AI Credit Scoring remains reliable over time and does not quietly fail or unfairly affect certain segments of society. By integrating privacy, security, and auditing into Credit Scoring Technology, organizations can establish high standards for responsible lending, making AI Credit Scoring not only more effective for risk management but also more transparent to consumers.

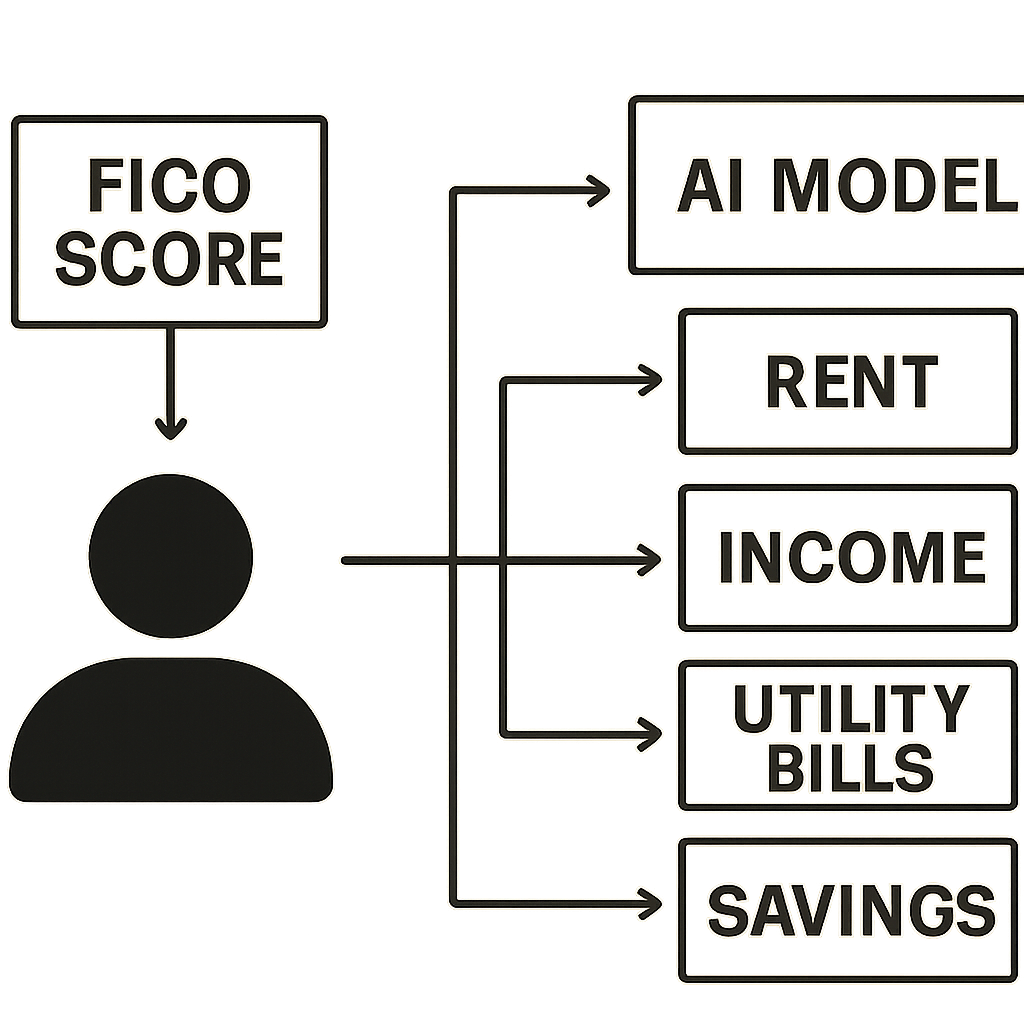

More Than Debt: The ‘Alternative Data’ That Can Unlock a Loan

When does an individual obtain a comprehensive “360-degree view”? When artificial intelligence, based on alternative data that most traditional scoring methods do not use, provides that view. Alternative data refers to all other forms of evidence of how a consumer manages their finances outside of debt and credit card usage.

Alternative data offers a new way for millions of consumers deemed “credit invisible”. Credit invisibles are individuals who consistently pay their bills on time and manage their finances effectively but lack a formal credit history. Many people in this group are young adults, recent immigrants, or those who prefer debit cards to credit cards. To the traditional scoring model, they appear to be a complete unknown. However, to an artificial intelligence model, they represent an opportunity to demonstrate reliability.

The opportunity for the artificial intelligence model to demonstrate the reliability of a credit invisible lies across multiple data sources. For example, when applying for a loan utilizing an advanced lending platform, a user may be required to provide secure access to their financial data, which would allow the model to identify additional forms of reliability, including:

• Payment history with regard to rent

• Utility bill payments (such as electricity or phone) made in a timely manner

• A consistent and positive cash flow from a bank account

• Education and/or employment history

For individuals who have consistently paid their rent on time over many years, this data finally recognizes their past responsible behavior. When this type of data is incorporated into machine learning models for loan applications, the system should be able to identify clear patterns of financial responsibility, even in the absence of a lengthy credit card history. While this alternative data improves the artificial intelligence model’s understanding, it also introduces a new form of risk: if the historical data used to train the model is inaccurate, what then?

Vendor’s Advanced AI Credit Scoring Integrated Tax Investment Bureau Data: Vendors use advanced AI credit scoring by integrating tax, investment, and bureau data for deeper risk assessment

Vendor’s Advanced AI Credit Scoring, Integrated with Tax Investment Bureau Data, describes a vendor-driven lending model that combines data from multiple verified sources to provide a clearer picture of the risk borrowers present.

A lender is able to assess the stability, capacity, and resiliency of an applicant through linking their bureau history with selected tax and investment information (as long as it is legal, and the applicant has given consent). A lender can better understand applicants in areas with limited information or where income and asset levels vary from one period to the next.

Vendor’s Advanced AI Credit Scoring Integrated Tax Investment Bureau Data can include items that would otherwise have to be analyzed separately, such as income consistency, employment and filing patterns, reported liabilities, and trends in investible assets, along with other bureau data points, including, but not limited to, utilization, payment history, and inquiries.

The vendors typically convert this input into time-based features (such as volatility and directional trend) and then use predictive models to estimate outcomes, such as the probability of delinquency. In addition, Vendor’s Advanced AI Credit Scoring Integrated Tax Investment Bureau Data will provide increased ranking power – identifying not only who is at high risk, but also why the risk may be increasing or decreasing.

However, having more information doesn’t automatically make your decisions better. The vendor’s Advanced AI Credit Scoring, Integrated with the Tax Investment Bureau Data, will require significant governance to ensure that only compliant, relevant, and explainable variables influence your decision-making.

In addition, the vendor’s Advanced AI Credit Scoring and the Integrated Tax Investment Bureau Data must be clearly sourced and include all applicable permissions, and the lender is responsible for ensuring that all vendors’ integrations meet the lender’s Privacy, Security, and Regulatory compliance requirements. Additionally, the vendor’s Advanced AI Credit Scoring and Integrated Tax Investment Bureau Data must include documentation of model validation, model drift monitoring, and fairness testing to ensure that no unintended disparate impacts arise from the use of the system.

Vendor’s Advanced AI Credit Scoring Integrated Tax Investment Bureau Data provides lenders with the ability to accurately determine approval levels, interest rates, and loan amounts, as well as improve channel consistency. In addition, the Vendor’s Advanced AI Credit Scoring, integrated with the Tax Investment Bureau Data, enables lenders to provide more detailed, auditable adverse action messages by producing clear, risk-driver-specific reason codes.

Therefore, when properly controlled, Vendor’s Advanced AI Credit Scoring, integrated with the Tax Investment Bureau Data, can provide lenders with a practical means to perform a more detailed risk assessment while balancing predictive performance with transparency and consumer trust.

The AI’s Blind Spot: How Can a Smart Machine Be Biased?

The problem isn’t the AI itself, but where it gets its knowledge. A mirror doesn’t know it’s a mirror, and neither does an AI model. The AI mirrors the world as it was taught; if the world it studied included decades of built-in inequalities in lending (and therefore, in history), then the AI will mirror those same inequalities. That is what we call algorithmic bias —the AI did not consciously decide to discriminate, but rather unintentionally copied the flaws of the past into a modern, high-tech form.

Ultimately, an AI is a machine that finds patterns. If it looks at millions of historical loan applications and determines that, based on “patterns,” people who live in a particular area were denied loans at a higher rate than others, and without recognizing that that denial was likely due to red-lining and other forms of discriminatory and outdated practices, the AI may draw the wrong conclusion. The AI may simply determine that people from that area have a higher risk of loan default and continue the same unjust practice using a new tool.

Developers even attempt to avoid this issue by instructing the AI to exclude protected characteristics, such as race or gender, from its decision-making. However, they do so at their own peril. The AI may identify a relationship between a particular zip code and loan defaults. As it turns out, the zip-code also happens to include a majority of the residents in that community.

While there is no apparent racial or ethnic component to the AI’s decision, it has identified a proxy for perpetuating the original discriminatory practice. This is known as proxy discrimination and is perhaps the greatest challenge to developing a completely equitable and fair system.

Building an Ethical Compass: How We Make AI Credit Scoring Fair

Developers do not simply rely upon the potential for an AI to be fair; rather, they make fairness a central part of how they develop an AI. In order to determine whether a developer has created a fair AI, the developer will test the AI multiple times during the development phase to identify whether the AI may have given more importance to certain data points (e.g., zip code) that could potentially be linked to a person’s race or gender.

This practice, known as Fair AI, is intended to develop an AI that does not give preference to prior inequalities, but instead bases decisions strictly upon an individual’s personal financial conduct.

In addition to developing an AI that is programmed to be fair, there should be evidence of the fairness of the AI. The explanation of this evidence is where the power of Explainable AI (XAI) becomes most relevant. XAI is similar to asking an AI to show you its work. Instead of receiving a simple yes or no answer from an AI, an XAI will provide a detailed explanation of why it made the decision it did.

For example, if an AI approves a loan based upon the fact that an applicant has consistently paid rent on time and has had a stable income over a period of time, the XAI will provide an explanation stating the basis of the decision was the applicant’s history of payment of rent and his/her history of employment.

The use of technical safeguards to prevent the creation of an AI that discriminates against individuals is further supported by federal and state regulations that prohibit credit discrimination. Examples of these regulations include the Equal Credit Opportunity Act (ECOA), which prohibits creditors from discriminating against applicants on the basis of race, color, religion, national origin, sex, marital status, age, or receipt of public assistance.

Additionally, many states have their own ECOA laws that regulate credit discrimination. These regulations were enacted before the advent of AI in the lending industry. As a result of these regulations, regulators require lenders to demonstrate that the AIs they use to evaluate credit applications are fair and comply with applicable laws and regulations. This provides an additional layer of human oversight of AI use in the lending industry.

Overall, the combination of active fairness testing, XAI, and regulation-based oversight forms a triad of checks and balances designed to produce a credit-scoring model that is not only more accurate than current models but also more equitable.

What AI Credit Scoring Means for You: More Approvals, Fairer Chances

For millions of people, this new approach will open avenues that were previously closed. The AI can now assess more data points (e.g., your rental history and consistent bank deposits) to provide a comprehensive view of your financial picture.

This represents a significant leap forward for financial inclusion – i.e., the notion that everyone should have access to financial tools on an equitable basis. Whether you’re a recent college grad who has landed a good job but doesn’t yet have a credit card, or you’re a reliable renter whose on-time rent payments have never been factored into a credit assessment, an AI system can take your financial stability into account and grant you the “yes” you deserve.

The new AI-based system for assessing creditworthiness offers a more realistic path to a second chance. Traditional credit scoring systems place heavy emphasis on past errors that can affect you for many years. In contrast, advanced AI-based credit scoring systems allow for greater focus to be placed on your current positive behaviors. For example, if you’ve paid all of your bills on time over the past year, they can assign more significance to that positive behavior than to a late payment made 5 years ago. The AI-based credit scoring system more accurately reflects your ability to continue improving.

In addition to being more equitable, the AI-based credit-scoring process is significantly faster. Rather than spending days waiting for a loan officer to manually review your file, an AI can render a decision in minutes. By eliminating the need for manual credit application reviews, the AI-based credit scoring system reduces uncertainty and anxiety associated with credit applications. Ultimately, this isn’t simply about a new type of credit score; it’s about developing a system that views each applicant individually.

Your Financial Story, Reimagined: How to Thrive in the New Era of Credit

Credit Risk Assessment is shifting from a single static number to a more fluid, inclusive view of an individual’s financial history. With the shift from being graded as a singular number to telling a complete story of who you are financially, you will have more control over how your story is told.

In order to make sure your story is portrayed fairly in this new world of credit assessment, you can begin to build your own financial story today by taking two simple steps:

1. Ask your landlord if he/she offers a rent reporting service so you may be able to receive credit for your timely rent payments.

2. Connect a secure third-party application (such as Plaid) to your banking information when you apply through a contemporary lender, so they will be able to see your income.

By completing these tasks, you provide lenders with a clearer picture of your overall financial situation, thereby improving financial inclusion for all. The future of credit is not about removing your past; it is about giving recognition to both your current and future potential. Which is a more accurate and fair way to tell the story of your financial history?

Conclusion

A new approach to understanding and providing credit, Fair & Advanced AI Credit Scoring uses advanced technology to view credit history as part of a broader picture of an individual’s financial situation.

The use of machine learning, combined with a wide range of indicators (rent and utilities, income, positive cash flow), enables a more comprehensive assessment of a borrower’s repayment capacity, thereby expanding access to more individuals, particularly those with no traditional credit history. Furthermore, this process may enable faster, more consistent loan processing and place greater emphasis on recent credit behavior rather than past credit behavior.

However, “Advanced” is only as good as the extent to which it is held accountable. AI systems will continue to perpetuate historical inequalities or discrimination by proxy unless fairness is built into their design from inception. Therefore, robust controls are necessary to ensure that AI systems operate fairly (e.g., by selecting appropriate data, testing for bias/disparate impact, providing explanations for decisions, monitoring for changes/drift in decision-making) and meet regulatory standards.

Therefore, the point is clear: the future of credit can be more inclusive and more accurate; however, only when lenders/vendors view fairness, transparency, and oversight as primary functions of their products will credit decisions be more intelligent and just.

FAQs

- What is AI credit scoring?

The use of machine-learning algorithms in the field of artificial intelligence (AI)- based credit scoring represents an improvement over conventional methods for assessing borrower risk by utilizing historical loan performance and a broader scope of financial data than those used in traditional credit scoring. - How is it different from a traditional FICO-style score?

The primary focus of traditional credit scoring has been credit bureau history, including payment history, debt, length of time since opening your first account, number of recent inquiries on your credit report, and the types of credit accounts you have established. The use of alternative data provides lenders with additional permissible sources beyond traditional credit reporting (e.g., rent and utility payments and bank cash-flow patterns) to obtain a more comprehensive picture of potential borrowers. - What is “alternative data,” and who benefits from it?

Alternative data refers to financial information that may not be reported in traditional credit reports. Alternative data can help “thin-file” and/or “credit-invisible” borrowers demonstrate their reliability and ability to repay a loan. - Can AI credit scoring be biased?

Yes. If historical lending data contain inequities, AI-based models can learn them and potentially replicate them through “proxy” variables (such as ZIP codes) that correlate with protected characteristics. - How do lenders make AI credit scoring fair and transparent? Fairness testing for disparate impact and limiting or removing risky variables, adding transparency to AI using explainable AI to allow for a clear understanding of how decisions were made, monitoring models for drift, and compliance with federal regulations such as the Equal Credit Opportunity Act are all measures that are being taken to mitigate unfair and discriminatory practices within the field of AI-based credit-scoring.

{kind=link}